PPP corridor: $4,885,300 principal → $4,933,228.76 forgiveness

Observed ERISA / ESOP vector: $1,200,000 ESOP receivable / stock-purchase pathway + $3,712,289 Savings Plan distribution outflow = $4,912,289

Classification: Receivable + stock purchase + distribution + investment appreciation ≠ employee salary ≠ payroll ≠ eligible PPP retirement-plan contribution as shown

Fully Integrated Primary-Source PPP / ERISA / ESOP Trace Memorandum

Subject: National PPP–ERISA–ESOP reduction, Selway’s unique public-record value signature, Savings Plan distribution pathway, ESOP receivable pathway, ESOP stock-purchase pathway, PPP eligibility consequence, Bayesian/combinatorial significance, and primary-document reconciliation demand.

Control status: This is the singular integrated memorandum. It incorporates the attached non-eligible-cost memo and revised Bayesian/combinatorial section into one sequenced memorandum rather than treating them as separate appendices.

I. Executive Conclusion

This analysis begins with two national public-record systems: Department of Labor / EBSA Form 5500 public filings and SBA PPP public loan-level data. DOL describes the Form 5500 Series as a compliance, research, disclosure, and data source for DOL, plan participants, beneficiaries, federal agencies, Congress, and the private sector; DOL also publishes raw Form 5500 datasets containing unedited filing and schedule data. (DOL) SBA publishes PPP public loan data in downloadable CSV format, including the public_150k_plus_240930.csv PPP FOIA file used in the public-data universe. (Small Business Administration)

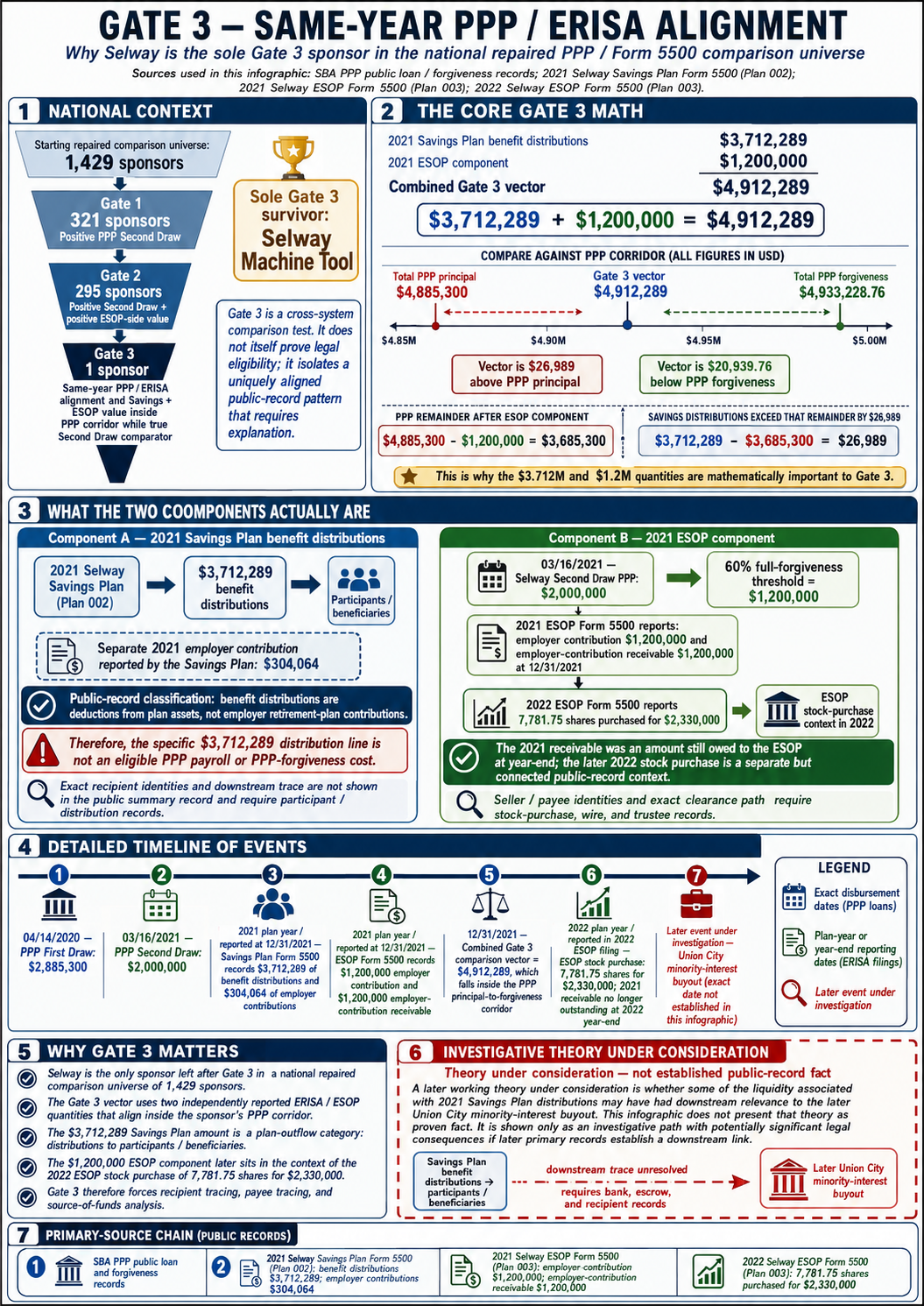

From that national public-record universe, the attached narrative states that the project reduced the relevant PPP, ERISA, Savings Plan, and ESOP-related fields into a repaired comparison universe of 6,431 analytical rows and 1,429 sponsors. The four-gate reduction then collapses the sponsor field from 1,429 sponsors → 321 positive Second Draw sponsors → 295 positive Second Draw plus positive ESOP sponsors → 1 true Second Draw same-year/corridor sponsor → 1 exact 60% Second Draw match. The sole surviving sponsor is Selway Machine Tool.

The core public-record value sequence is:

| PPP First Draw |

$2,885,300 |

| PPP Second Draw |

$2,000,000 |

| Total PPP principal |

$4,885,300 |

| PPP forgiveness total |

$4,933,228.76 |

| Public payroll-coded proceeds |

$4,885,297 |

| Public nonpayroll residue |

$3 |

| 60% of Second Draw |

$1,200,000 |

| 2021 ESOP employer contribution receivable |

$1,200,000 |

| 2021 Savings Plan benefit distributions |

$3,712,289 |

| Combined native ERISA / ESOP vector |

$4,912,289 |

| Difference from PPP principal |

$26,989 |

| Difference from PPP forgiveness |

$20,939.76 |

| 2022 ESOP stock purchase |

$2,330,000 |

The 2021 ESOP filing reports both $1,200,000 employer contribution and $1,200,000 employer contribution receivable; the prior-year comparative receivable was only $100,000. The 2021 Savings Plan filing reports $3,712,289 in benefit distributions and separately reports employer contributions of only $304,064, confirming that the $3.712M amount is a distribution outflow rather than an employer contribution. The 2022 ESOP filing then shows employer contributions receivable reduced from $1,200,000 in 2021 to zero in 2022, and separately reports a $2,330,000 purchase of 7,781.75 shares of Selway common stock.

The public filings therefore support a two-lane ERISA / ESOP value trace:

- Savings Plan exit lane: $3,712,289 in 2021 benefit distributions.

- ESOP employer-stock lane: $1,200,000 employer contribution receivable in 2021, cleared by 2022, followed by a $2,330,000 ESOP purchase of Selway common stock.

The mapped ERISA / ESOP categories are not PPP eligible payroll costs as shown. A Savings Plan benefit distribution is a plan outflow. An ESOP employer contribution receivable is not payment proof. A purchase of company common stock is not payroll. SBA/Treasury Form 3508 instructions require payment receipts, cancelled checks, or account statements documenting employer retirement-plan contributions included in forgiveness. (U.S. Department of the Treasury)

This does not prove PPP fraud, false certification, or cash misuse by itself. It proves a nationally unique, document-dependent reconciliation problem: if Selway’s forgiveness files relied on any of these ERISA / ESOP values, the public record creates a material eligibility, timing, classification, and documentation issue requiring primary records.

II. Public Source Foundation

The analysis rests on two separate public systems.

First, the DOL / EBSA Form 5500 system provides public employee-benefit-plan filings, including financial schedules, plan identity, sponsor identity, assets, liabilities, contributions, distributions, party-in-interest transactions, and Schedule H data. DOL identifies Form 5500 raw datasets as unedited data from all filings for each year, including schedule data. (DOL)

Second, the SBA PPP public loan-level system provides borrower-level PPP data. SBA’s public PPP data page states that all PPP loan data is available in CSV format, and the SBA data portal identifies the PPP FOIA public_150k_plus_240930.csv file as a public-domain CSV resource. (Small Business Administration)

The attached narrative states that the public source universe under examination contained approximately:

| Form 5500 / ERISA public rows |

2,030,185 |

| PPP public rows |

968,524 |

| Total public-record rows |

2,998,709 |

Those raw public-record sources were reduced into a repaired analytical comparison universe of 6,431 analytical rows and 1,429 sponsors.

III. National Four-Gate Reduction

The national reduction does not begin by asking whether Selway looks suspicious. It asks whether any sponsor in the national comparison universe satisfies the same objective public-record conditions.

Gate 1 — Positive PPP Second Draw

This gate asks whether the sponsor has a positive PPP Second Draw amount. The 60% Second Draw threshold cannot be applied to a borrower that did not have a positive Second Draw.

| Repaired comparison universe |

1,429 |

| Positive PPP Second Draw |

321 |

Gate 1 narrows the universe from 1,429 to 321 sponsors.

Gate 2 — Positive Second Draw plus positive ESOP-side value

This gate requires both sides of the comparison: a positive PPP Second Draw and a positive ESOP-side value.

| Positive PPP Second Draw |

321 |

| Positive Second Draw + positive ESOP |

295 |

Gate 2 narrows the true comparator field from 321 to 295 sponsors.

Gate 3 — Same-year PPP / ERISA alignment and corridor placement

This gate asks whether the sponsor has same-year PPP / ERISA alignment and whether the combined Savings Plan plus ESOP value falls inside the same borrower’s PPP principal-to-forgiveness corridor while remaining a true Second Draw comparator.

The attached narrative states that the broader same-year/corridor/Savings-plus-ESOP test identified 11 rows / 11 sponsors, but the corrected Second Draw denominator is decisive: of those apparent near-comparators, only one had a positive Second Draw. The others had second_draw_current = 0, meaning they were not true Second Draw threshold comparators.

Within the corrected denominator, Gate 3 reduces the field to one sponsor: Selway Machine Tool.

Gate 4 — Exact ESOP component equals 60% of PPP Second Draw

This gate asks whether the ESOP component equals exactly 60% of the sponsor’s PPP Second Draw.

For Selway:

| PPP Second Draw |

$2,000,000 |

| 60% of Second Draw |

$1,200,000 |

| ESOP component |

$1,200,000 |

| Deviation |

$0 |

| Percent deviation |

0% |

The arithmetic is direct:

$2,000,000 × 60% = $1,200,000

Gate 4 confirms that the sole surviving true Second Draw comparator also has the exact 60% match.

IV. National Reduction Summary

| Starting comparison universe |

Sponsors derived from national PPP, ERISA, Savings Plan, and ESOP-related public records |

1,429 |

| Gate 1 |

Positive PPP Second Draw? |

321 |

| Gate 2 |

Positive Second Draw plus positive ESOP-side value? |

295 |

| Gate 3 |

Same-year PPP / ERISA alignment and Savings Plan + ESOP value inside PPP corridor while remaining a true Second Draw comparator? |

1 |

| Gate 4 |

ESOP component exactly equals 60% of Second Draw? |

1 |

The final result is one surviving sponsor: Selway Machine Tool.

The public-record finding is not that Selway merely had PPP and a retirement plan. The finding is that Selway is the only true Second Draw sponsor in the tested national comparison universe whose public records show positive Second Draw, positive ESOP, same-year PPP / ERISA corridor alignment, combined Savings Plan plus ESOP value inside the PPP corridor, and exact ESOP-to-Second-Draw 60% matching.

V. Selway PPP Value Signature

The attached narrative states Selway’s public PPP value signature as follows:

| First Draw current |

$2,885,300 |

| Second Draw current |

$2,000,000 |

| PPP current total / principal |

$4,885,300 |

| PPP forgiveness total |

$4,933,228.76 |

| Payroll proceed total |

$4,885,297 |

| Nonpayroll residue |

$3 |

| Second Draw 60% target |

$1,200,000 |

| Second Draw 60% deviation |

0% |

The public payroll coding ratio is:

$4,885,297 / $4,885,300 = 99.99994%

That is important because the public PPP story is nearly entirely payroll-coded, while the public ERISA / ESOP value trace resolves into Savings Plan distributions, ESOP receivable mechanics, and ESOP employer-stock purchase mechanics.

VI. 2021 Savings Plan Distribution Lane

The 2021 Selway Savings Plan statement of changes reports:

| Employee contributions |

$1,216,257 |

| Employer contributions |

$304,064 |

| Rollovers from qualified plans |

$262 |

| Total contributions |

$1,520,583 |

| Net appreciation in fair value of investments |

$2,677,270 |

| Interest income on notes receivable from participants |

$22,166 |

| Total additions |

$4,220,019 |

| Benefit distributions |

$3,712,289 |

| Administration fees |

$65,640 |

| Total deductions |

$3,777,929 |

| Net increase |

$442,090 |

| End net assets |

$21,403,648 |

The critical category distinction is that $3,712,289 is not an employer contribution. Employer contributions were only $304,064. The $3,712,289 value is a benefit-distribution deduction: a plan outflow to participants or beneficiaries.

Therefore, the Savings Plan lane is:

ERISA plan outflow → benefit distribution → not borrower-paid payroll → not employer retirement-plan contribution payment → not PPP payroll cost as shown.

VII. 2021 ESOP Receivable Lane

The 2021 Selway ESOP statement of net assets reports:

| Investment in plan sponsor common stock, fair value |

$6,718,174 |

$6,497,221 |

| Cash |

$1,964,234 |

$2,005,120 |

| Employer contribution receivable |

$1,200,000 |

$100,000 |

| Total assets |

$9,882,408 |

$8,602,341 |

| Net assets available for benefits |

$9,860,588 |

$8,579,858 |

The same 2021 ESOP statement of changes reports:

| Net appreciation in fair value of investments |

$220,953 |

| Employer contribution |

$1,200,000 |

| Total additions |

$1,420,953 |

| Benefit distributions |

$140,223 |

| Net increase |

$1,280,730 |

The 2021 ESOP filing therefore shows both:

Employer contribution = $1,200,000 Employer contribution receivable = $1,200,000

That distinction is controlling. A receivable is an asset claim against the employer. It is not proof that cash was paid into the ESOP during the PPP covered period.

The amount is also exactly equal to the Second Draw 60% threshold:

$2,000,000 × 60% = $1,200,000

Thus, the 2021 ESOP lane is simultaneously:

- an ESOP employer contribution value;

- an ESOP employer contribution receivable;

- a value exactly equal to 60% of Selway’s Second Draw; and

- not payment proof on the public record.

VIII. PPP Remainder After ESOP Receivable

The next step is to isolate the ESOP receivable from total PPP principal:

| Total PPP principal |

$4,885,300 |

| Less ESOP employer contribution receivable |

$1,200,000 |

| PPP remainder after ESOP receivable |

$3,685,300 |

Compare that remainder to the 2021 Savings Plan distribution lane:

| 2021 Savings Plan benefit distributions |

$3,712,289 |

| PPP remainder after ESOP receivable |

$3,685,300 |

| Difference |

$26,989 |

The deviation is:

$26,989 / $3,685,300 = 0.73234%

So the Savings Plan distribution event equals 100.73234% of the PPP remainder after the ESOP receivable is removed.

This does not prove dollar-for-dollar cash movement. It proves a highly specific public-record value convergence: once the ESOP $1.2M lane is isolated, the remaining PPP principal is nearly matched by the 2021 Savings Plan distribution lane.

IX. Combined ERISA / ESOP Vector

Using the native 2021 Savings Plan PDF value, the combined ERISA / ESOP vector is:

| 2021 Savings Plan benefit distributions |

$3,712,289 |

| 2021 ESOP employer contribution receivable |

$1,200,000 |

| Combined ERISA / ESOP vector |

$4,912,289 |

Compare to PPP principal:

| Distance above PPP principal |

$4,912,289 − $4,885,300 |

$26,989 |

| Percent above PPP principal |

$26,989 / $4,885,300 |

0.55245% |

| Combined vector as percent of PPP principal |

$4,912,289 / $4,885,300 |

100.55245% |

Compare to PPP forgiveness:

| Distance below PPP forgiveness |

$4,933,228.76 − $4,912,289 |

$20,939.76 |

| Percent below PPP forgiveness |

$20,939.76 / $4,933,228.76 |

0.42446% |

| Combined vector as percent of PPP forgiveness |

$4,912,289 / $4,933,228.76 |

99.57554% |

This is the combined vector significance: the native ERISA / ESOP vector falls inside Selway’s PPP principal-to-forgiveness corridor, only $26,989 above principal and $20,939.76 below forgiveness.

X. 2022 ESOP Receivable Clearance and Stock-Purchase Pathway

The 2022 ESOP statement of net assets shows:

| Investment, at fair value |

$9,079,790 |

$6,718,174 |

| Employer contributions receivable |

— |

$1,200,000 |

| Non-interest-bearing cash |

$909,992 |

$1,964,234 |

| Total assets |

$9,989,782 |

$9,882,408 |

| Net assets available for benefits |

$9,989,782 |

$9,860,588 |

This shows the employer contribution receivable was present at $1,200,000 in 2021 and reduced to zero in 2022.

The 2022 ESOP statement of changes reports:

| Unrealized appreciation in fair value of investment |

$31,616 |

| Dividends |

$267,985 |

| Employer contributions |

$150,000 |

| Total additions |

$449,601 |

| Benefits paid to participants |

$320,323 |

| Administrative expenses |

$84 |

| Net increase |

$129,194 |

This matters because the 2022 employer contribution amount is only $150,000, while the 2021 $1,200,000 receivable was cleared.

The 2022 ESOP Schedule H Line 4i reports:

| 30,350.95 shares of Selway common stock |

$10,127,671 |

$9,079,790 |

The 2022 Schedule H Line 4j reports a purchase of:

| Selway Machine Tool Co., Inc. |

Purchase of 7,781.75 shares of common stock |

$2,330,000 |

The transaction-date current value and cost are both shown as $2,330,000.

The 2021-to-2022 share movement ties exactly:

| 2021 ESOP common shares |

22,569.20 |

| 2022 ESOP common shares |

30,350.95 |

| Increase |

7,781.75 |

That increase equals the reported 2022 purchase quantity.

The public ESOP sequence is therefore:

2021: ESOP books $1,200,000 employer contribution receivable. 12/31/2021: Receivable remains outstanding. 2022: Receivable clears to zero. 2022: ESOP purchases $2,330,000 of Selway common stock. 12/31/2022: ESOP share count increases by exactly 7,781.75 shares.

That is the employer-stock transaction pathway.

XI. PPP Eligibility Consequence

The mapped ERISA / ESOP categories are not PPP eligible payroll costs as shown.

1. Savings Plan benefit distributions

The $3,712,289 amount is a benefit distribution. It is a plan outflow to participants or beneficiaries. It is not borrower-paid payroll, not employer retirement contribution, and not cash compensation paid by the borrower during the covered period. The same Savings Plan filing separately reports employer contributions of only $304,064.

2. ESOP employer contribution receivable

The $1,200,000 ESOP amount is a receivable at year-end 2021. A receivable is not a payment receipt, cancelled check, account statement, wire, ACH, or ESOP trust receipt.

SBA/Treasury Form 3508 instructions require documentation such as payment receipts, cancelled checks, or account statements documenting employer contributions to employee retirement plans included in forgiveness. (U.S. Department of the Treasury)

Therefore, a year-end ESOP receivable does not satisfy the payment-documentation standard by itself. If Selway counted the $1,200,000 amount for PPP forgiveness, Selway must produce contrary transaction-level evidence proving eligibility, timing, payment/incurrence, documentation, and no double counting.

3. ESOP purchase of Selway common stock

The $2,330,000 ESOP transaction is a purchase of company common stock. It is an ESOP employer-stock investment transaction. It is not payroll, not borrower-paid compensation, and not an employer retirement-plan contribution payment.

Thus, the public ERISA / ESOP trace does not support PPP eligibility. It supports the opposite: the PPP-sized public value corridor maps into categories that are non-payroll as shown.

XII. Integrated Timeline

Phase 1 — National public-data universe

DOL Form 5500 public datasets and SBA PPP public loan-level datasets are staged. DOL provides Form 5500 raw filing and schedule data; SBA provides PPP public loan CSV data. (DOL)

Phase 2 — Repaired comparison universe

The attached narrative states that the public-record universe is reduced to 6,431 analytical rows and 1,429 sponsors.

Phase 3 — Four-gate reduction

The sponsor field narrows:

1,429 → 321 → 295 → 1 → 1

That one sponsor is Selway Machine Tool.

Phase 4 — PPP value corridor

Selway’s PPP values are:

First Draw: $2,885,300 Second Draw: $2,000,000 PPP principal: $4,885,300 PPP forgiveness: $4,933,228.76 Payroll-coded proceeds: $4,885,297 Nonpayroll residue: $3

Phase 5 — 2021 Savings Plan

The Savings Plan reports $3,712,289 in benefit distributions and only $304,064 in employer contributions.

Phase 6 — 2021 ESOP

The ESOP reports $1,200,000 employer contribution and $1,200,000 employer contribution receivable.

Phase 7 — PPP remainder

$4,885,300 − $1,200,000 = $3,685,300

Phase 8 — Combined ERISA / ESOP vector

$3,712,289 + $1,200,000 = $4,912,289

This is within $26,989 of PPP principal and within $20,939.76 of PPP forgiveness.

Phase 9 — 2022 ESOP clearance and stock purchase

The ESOP receivable clears by 2022, and the ESOP purchases 7,781.75 shares of Selway common stock for $2,330,000.

Phase 10 — Document demand

The public records establish value convergence, timing sequence, category mismatch, and related-party ESOP stock mechanics. They do not prove exact bank movement or intent. The next layer is primary PPP, payroll, bank, Savings Plan, ESOP, trust, valuation, stock-purchase, tax, and accounting records.

XIII. Bayesian and Combinatorial Significance — Fully Integrated and Recalculated

The Bayesian and combinatorial significance of the Selway finding must be stated carefully. This analysis does not assume that every gate is statistically independent. Some gates are logically related. For example, the exact 60% Second Draw test depends on the sponsor having a positive Second Draw in the first place. Therefore, the correct framing is not naïve multiplication. The correct framing is empirical survival probability, conditional narrowing, corridor-fit significance, Bayesian likelihood comparison, and combinatorial stacking across separate public-record systems.

XIII.A. Empirical survival probability

The observed national reduction is:

| Repaired sponsor universe |

1 |

1,429 |

0.06998% |

| True positive Second Draw sponsors |

1 |

321 |

0.31153% |

| Positive Second Draw + positive ESOP sponsors |

1 |

295 |

0.33898% |

These are not theoretical probabilities. They are observed survival rates inside the constructed national comparison universe. The strongest denominator is the true Second Draw comparator universe, because the 60% threshold question only has meaning for sponsors with a positive Second Draw.

From that corrected comparator group, the result is:

1 surviving sponsor out of 321 true Second Draw sponsors: Selway Machine Tool.

XIII.B. Conditional narrowing sequence

| Positive Second Draw among all repaired sponsors |

1,429 → 321 |

22.4633% |

| Positive ESOP among positive Second Draw sponsors |

321 → 295 |

91.9003% |

| Same-year/corridor/Savings+ESOP convergence among positive Second Draw + ESOP sponsors |

295 → 1 |

0.33898% |

| Exact 60% Second Draw match after corrected convergence |

1 → 1 |

100% confirmatory |

The key collapse occurs at the same-year/corridor/Savings-plus-ESOP convergence gate, where the field moves from 295 sponsors to 1 sponsor. Gate 4 then confirms that the only surviving sponsor also has the exact 60% Second Draw match.

Gate 4 should not be treated as an independent statistical event. It is better understood as a confirmatory precision marker: after the corrected denominator is applied, there are no true Second Draw sponsors that pass the same-year/corridor/Savings+ESOP convergence test and then fail the exact 60% test.

The observed count is:

G1 + G2 + G3 with positive Second Draw but failing G4 = 0

That matters because the national comparison universe does not reveal a class of similar true Second Draw sponsors. It reveals Selway alone.

XIII.C. PPP corridor-fit recalculation

The integrated memo uses the native 2021 Savings Plan PDF value of $3,712,289, not the prior repaired dataset value of $3,712,443. The 2021 Savings Plan filing shows benefit distributions of $3,712,289 and separately shows employer contributions of $304,064, confirming that the $3.712M value is a distribution outflow rather than an employer contribution.

The 2021 ESOP filing shows $1,200,000 employer contribution and $1,200,000 employer contribution receivable.

The recalculated native-source ERISA / ESOP vector is:

| 2021 Savings Plan benefit distributions |

$3,712,289 |

| 2021 ESOP employer contribution receivable |

$1,200,000 |

| Combined ERISA / ESOP vector |

$4,912,289 |

The PPP values are:

| PPP principal |

$4,885,300 |

| PPP forgiveness |

$4,933,228.76 |

| PPP corridor width |

$47,928.76 |

The combined ERISA / ESOP vector falls inside the PPP principal-to-forgiveness corridor:

| Distance above PPP principal |

$4,912,289 − $4,885,300 |

$26,989 |

| Distance below PPP forgiveness |

$4,933,228.76 − $4,912,289 |

$20,939.76 |

| Percent above PPP principal |

$26,989 / $4,885,300 |

0.55245% |

| Percent below PPP forgiveness |

$20,939.76 / $4,933,228.76 |

0.42446% |

| Combined vector as percent of PPP principal |

$4,912,289 / $4,885,300 |

100.55245% |

| Combined vector as percent of PPP forgiveness |

$4,912,289 / $4,933,228.76 |

99.57554% |

This is the Phase 8 significance: the combined ERISA / ESOP vector does not merely approximate a random number. It lands inside the borrower’s PPP principal-to-forgiveness corridor, only $26,989 above principal and only $20,939.76 below forgiveness.

XIII.D. Remainder trace recalculation

After isolating the ESOP receivable from PPP principal:

| PPP principal |

$4,885,300 |

| Less ESOP receivable |

$1,200,000 |

| PPP remainder after ESOP receivable |

$3,685,300 |

Compare that remainder to the 2021 Savings Plan distribution lane:

| 2021 Savings Plan benefit distributions |

$3,712,289 |

| PPP remainder after ESOP receivable |

$3,685,300 |

| Difference |

$26,989 |

The deviation is:

$26,989 / $3,685,300 = 0.73234%

So the Savings Plan distribution event is 100.73234% of the PPP remainder after the ESOP receivable is removed. This is a second convergence layer: the first convergence is the combined ERISA / ESOP vector inside the PPP principal-to-forgiveness corridor; the second convergence is the Savings Plan distribution amount nearly equaling the remaining PPP principal after the ESOP receivable lane is isolated.

XIII.E. Exact Second Draw 60% marker

Selway’s Second Draw was $2,000,000. The PPP payroll-cost threshold is tied to the 60% payroll-cost rule; Form 3508 implements the payroll-cost threshold in the forgiveness calculation by comparing eligible payroll costs against the 60% requirement. (U.S. Department of the Treasury)

For Selway:

| Second Draw |

$2,000,000 |

| 60% of Second Draw |

$1,200,000 |

| 2021 ESOP component / receivable |

$1,200,000 |

| Deviation |

$0 |

| Percent deviation |

0% |

This exact match is not proof of misuse by itself. But in Bayesian terms it is a high-salience precision marker because it connects the ESOP receivable amount to the PPP Second Draw payroll-threshold amount with no rounding deviation. The significance increases because the $1,200,000 appears in the ESOP filing as a receivable at 12/31/2021, not as documented cash payment proof.

XIII.F. Additional 2022 ESOP follow-through

The Bayesian weight also increases because the 2021 ESOP receivable is not an isolated static entry. The 2022 ESOP filing shows a follow-on employer-stock transaction pathway.

The 2022 ESOP filing reports a purchase of 7,781.75 shares of Selway common stock for $2,330,000.

The share movement ties out:

| 2021 ESOP common shares |

22,569.20 |

| 2022 ESOP common shares |

30,350.95 |

| Increase |

7,781.75 |

The increase equals the reported 2022 purchase quantity.

This adds sequence and direction to the pattern:

2021 ESOP receivable → receivable clearance pathway → 2022 ESOP purchase of Selway common stock → exact share-count tie-out.

That is not the same as a single-year accounting anomaly. It is a multi-year ERISA / ESOP transaction sequence.

XIII.G. Payroll-coding tension

The attached narrative states that Selway’s public PPP proceeds were almost entirely payroll-coded:

| Payroll proceed total |

$4,885,297 |

| PPP principal |

$4,885,300 |

| Nonpayroll residue |

$3 |

That is:

$4,885,297 / $4,885,300 = 99.99994% payroll-coded

The tension is that the public PPP story is nearly all payroll-coded, while the public ERISA / ESOP value trace resolves into:

- Savings Plan benefit distributions;

- ESOP employer contribution receivable; and

- ESOP purchase of employer common stock.

Those categories are not ordinary payroll categories. They are not PPP eligible payroll costs as shown. The Bayesian significance increases because the public coding and the public ERISA / ESOP value trace point in different categorical directions.

XIII.H. Bayesian hypotheses

The Bayesian comparison is between two explanatory models.

Hypothesis A — Benign coincidence / ordinary administration

Under the benign hypothesis, the observed pattern is coincidental or administratively ordinary. This hypothesis requires that all of the following be true or benignly explainable:

- Selway’s survival as the only sponsor after the corrected national gate sequence is coincidental.

- The $1,200,000 ESOP receivable exactly matching 60% of the $2,000,000 Second Draw is coincidental or unrelated to PPP threshold logic.

- The $3,712,289 Savings Plan distribution amount nearly equaling the PPP remainder after ESOP receivable is coincidental.

- The combined $4,912,289 ERISA / ESOP vector falling inside the $4,885,300 to $4,933,228.76 PPP corridor is coincidental.

- The near-total payroll-coded PPP proceeds are independently and fully supported by ordinary payroll records.

- The $1,200,000 ESOP receivable was excluded from forgiveness, or if included, was eligible, timely, paid/incurred, and documented.

- The Savings Plan distributions were not used as borrower-paid payroll support.

- The 2022 ESOP stock purchase was unrelated to the 2021 receivable and PPP-value convergence.

- No double counting, misclassification, or timing mismatch occurred.

- The PPP forgiveness certifications were true and complete.

This hypothesis remains possible, but it is document-dependent.

Hypothesis B — Material reconciliation concern

Under the reconciliation-concern hypothesis, the observed pattern reflects a material public-record reconciliation problem requiring primary documents.

This hypothesis is supported by the following observed features:

- Selway is the only surviving sponsor under the corrected national gate sequence.

- Selway is a true Second Draw comparator.

- Selway has a positive ESOP component.

- The ESOP component exactly equals 60% of the Second Draw.

- Selway has a large same-year Savings Plan distribution lane.

- The Savings Plan distribution amount nearly equals the PPP remainder after removing the ESOP receivable.

- The combined ERISA / ESOP vector falls inside the PPP principal-to-forgiveness corridor.

- PPP public proceeds are nearly all payroll-coded.

- The 2021 ESOP $1,200,000 is a receivable, not payment proof.

- The receivable is followed by a 2022 ESOP stock-purchase pathway.

- The mapped ERISA / ESOP categories are not PPP eligible payroll costs as shown.

This hypothesis does not prove fraud. It says the public record creates a specific, high-probative-value reconciliation demand.

XIII.I. Likelihood-ratio logic

In Bayesian terms:

Posterior odds = Prior odds × Likelihood ratio

The likelihood ratio compares:

P(observed pattern | benign coincidence) against P(observed pattern | material reconciliation concern)

The observed pattern is:

E = {positive Second Draw, positive ESOP, same-year PPP / ERISA alignment, Savings Plan + ESOP vector inside PPP corridor, exact ESOP = 60% of Second Draw, near-total payroll coding, ESOP receivable rather than payment proof, later ESOP stock purchase, share-count tie-out}.

The benign model must explain every element of E as ordinary, unrelated, or properly documented. The reconciliation-concern model explains E as a mutually reinforcing set of public-record indicators pointing to a missing primary-document reconciliation.

The likelihood ratio is not assigned a numeric value here because the required base-rate distributions and dependence structure are not fully established. But the direction of Bayesian movement is clear: the observed evidence materially increases the posterior probability that the primary documents are probative and necessary.

XIII.J. Combinatorial significance

The combinatorial significance is that Selway is not identified by one unusual number. Selway is identified by a stacked public-record sequence across distinct categories:

- PPP borrower data.

- PPP First Draw and Second Draw values.

- PPP payroll-coded proceeds.

- PPP principal-to-forgiveness corridor.

- ERISA / Form 5500 plan reporting.

- Savings Plan benefit distributions.

- ESOP employer contribution receivable.

- ESOP employer-stock investment.

- Same-year timing.

- Exact 60% Second Draw threshold matching.

- 2022 receivable-clearance / stock-purchase pathway.

- 7,781.75-share tie-out.

The combinatorial event is not:

“Selway had PPP and a retirement plan.”

The combinatorial event is:

“Selway is the only true Second Draw sponsor in the national comparison universe whose public records show positive Second Draw, positive ESOP, same-year PPP / ERISA alignment, Savings Plan plus ESOP value inside the PPP principal-to-forgiveness corridor, exact ESOP component equal to 60% of Second Draw, near-total payroll coding, and a follow-on ESOP stock-purchase pathway.”

That is the public-record significance.

XIII.K. Revised Bayesian conclusion

The public-record pattern is empirically rare, conditionally concentrated, corridor-specific, and category-significant. Selway survives a national reduction from 1,429 sponsors to one sponsor, and from 321 true Second Draw sponsors to one sponsor. The ESOP component exactly equals 60% of the Second Draw. The native-source combined ERISA / ESOP vector equals $4,912,289, which falls inside the PPP principal-to-forgiveness corridor: $26,989 above PPP principal and $20,939.76 below PPP forgiveness. The Savings Plan distribution amount is only $26,989 above the PPP remainder after isolating the ESOP receivable. The 2022 ESOP filing then shows a $2,330,000 purchase of Selway common stock, with a share-count increase matching the reported purchase quantity.

This does not prove PPP fraud, false certification, or cash misuse by itself. It does prove that the observed public-record pattern has substantial Bayesian and combinatorial significance. The appropriate conclusion is that Selway’s PPP forgiveness files, payroll records, bank records, Savings Plan records, ESOP receivable records, ESOP trust records, and stock-purchase documents have high probative value and are necessary to resolve the reconciliation question.

XIV. What Must Be True for the PPP Forgiveness Files Not to Contain Material False Statements

For Selway’s First Draw and Second Draw forgiveness files to be fully supportable, the primary records must show:

- Selway was eligible for the First Draw and Second Draw PPP loans.

- The First Draw and Second Draw loan amounts were correctly calculated.

- Forgiveness was supported by eligible costs.

- Payroll costs were paid or incurred during the applicable covered periods.

- At least 60% of Second Draw forgiveness support consisted of eligible payroll costs.

- Any retirement-plan costs included in forgiveness were actual eligible employer costs.

- Any retirement-plan costs included in forgiveness were paid or incurred within PPP timing rules.

- Retirement-plan costs included in forgiveness were documented by receipts, cancelled checks, account statements, or equivalent trust/payment records.

- The $1,200,000 ESOP receivable was either excluded from forgiveness or fully supported by legally sufficient contrary proof.

- The $3,712,289 Savings Plan distributions were not treated as borrower-paid payroll costs.

- The $2,330,000 ESOP stock purchase was not treated as payroll or retirement-plan contribution cost.

- No value was double-counted across payroll, retirement contribution, ESOP reporting, Savings Plan distributions, tax deductions, Form 5500 reporting, or PPP forgiveness.

- Borrower certifications were true, complete, and supported by records when made.

The critical unresolved question is:

Was the $1,200,000 ESOP component included, excluded, or independent from the Second Draw forgiveness support?

The public filings do not answer that question. The primary documents must.

XV. Primary Documents Required

To resolve the issue conclusively, the following primary records are required.

PPP First Draw: First Draw application, borrower certifications, note, disbursement record, covered-period election, forgiveness application, Form 3508/3508EZ/3508S, Schedule A, Schedule A worksheet, lender review file, SBA forgiveness decision, forgiveness payment record, and lender communications.

PPP Second Draw: Second Draw application, revenue-reduction support, borrower certifications, note, disbursement record, covered-period election, forgiveness application, Form 3508/3508EZ/3508S, Schedule A, Schedule A worksheet, Schedule A Line 7 support, lender review file, SBA forgiveness decision, forgiveness payment record, and lender communications.

Payroll and tax: Payroll registers, payroll processor reports, Forms 941, W-2, W-3, employee-level wage detail, owner/officer compensation calculations, FTE worksheets, salary/hourly wage reduction worksheets, payroll bank disbursements, payroll journal entries, and payroll-to-GL mappings.

Bank and cash records: PPP deposit account statements, payroll disbursement account statements, ACH confirmations, wire confirmations, check registers, transfer records, general ledger cash accounts, retirement expense accounts, accrued contribution accounts, ESOP payable/receivable accounts, and records showing whether PPP proceeds were segregated or commingled.

Savings Plan records: Plan document, trust agreement, trust statements, participant-level distribution ledger, distribution dates, distribution authorizations, Forms 1099-R, rollover records, distribution bank records, plan administrator workpapers, year-end asset reconciliation, and year-end distribution reconciliation.

ESOP records: ESOP plan document, trust agreement, ESOP trust statements, contribution ledger, employer contribution receivable schedule, employer payable ledger, documents showing whether the $1,200,000 was paid/accrued/offset/converted/netted, stock purchase agreement, seller/payee identity, wire/check records, ESOP valuation reports, trustee approvals, board approvals, stock ledger, and stock certificates.

Form 5500 / ERISA filing records: Original and amended Form 5500 filings, Schedule H workpapers, original-vs-amended deltas, EFAST metadata, signer authorization records, Joseph Madden signature/support records, preparer communications, plan administrator workpapers, and communications among Selway, lender, payroll provider, CPA, plan administrator, ESOP trustee, Savings Plan trustee, and counsel.

This analysis begins with national public records: DOL / EBSA Form 5500 filings and SBA PPP public loan-level data. From the public-record universe described in the attached narrative, the project created a repaired comparison universe of 6,431 analytical rows and 1,429 sponsors. Four objective gates reduce that universe from 1,429 sponsors to 321 positive Second Draw sponsors, then to 295 sponsors with positive Second Draw plus positive ESOP-side values, then to one true Second Draw sponsor with same-year PPP / ERISA alignment and Savings Plan plus ESOP value inside the PPP corridor, and finally to one sponsor whose ESOP component exactly equals 60% of the Second Draw. That sponsor is Selway Machine Tool.

Selway’s PPP principal was $4,885,300 and total forgiveness was $4,933,228.76. Public PPP data in the attached narrative shows payroll proceeds of $4,885,297, leaving only $3 outside payroll coding. Selway’s Second Draw was $2,000,000; 60% of that amount is $1,200,000. The 2021 ESOP filing shows a $1,200,000 employer contribution and a $1,200,000 employer contribution receivable at 12/31/2021. A receivable is an asset claim against the employer, not proof of cash payment into the ESOP during the PPP covered period.

After removing the $1,200,000 ESOP receivable from total PPP principal, the remaining PPP principal is $3,685,300. The 2021 Savings Plan reports $3,712,289 in benefit distributions, only $26,989 above that remainder. The combined native ERISA / ESOP vector is $3,712,289 + $1,200,000 = $4,912,289, within approximately 0.552% of PPP principal and within $20,939.76 of total forgiveness.

The 2022 ESOP filing then reports a $2,330,000 purchase of 7,781.75 shares of Selway common stock. The ESOP share count increased from 22,569.20 shares in 2021 to 30,350.95 shares in 2022, an increase of exactly 7,781.75 shares, matching the reported purchase quantity.

The mapped ERISA / ESOP categories are not PPP eligible payroll costs as shown. The Savings Plan amount is a benefit-distribution outflow, not borrower-paid payroll or employer contribution. The ESOP $1,200,000 amount is a receivable, not documented covered-period payment proof. The ESOP $2,330,000 stock transaction is a purchase of company common stock, not payroll or employer retirement-plan contribution payment. SBA/Treasury PPP instructions require payment receipts, cancelled checks, or account statements to document employer retirement-plan contributions included in forgiveness. (U.S. Department of the Treasury)

Accordingly, the public filings support a fully integrated PPP / ERISA / ESOP reconciliation problem requiring transaction-level PPP, payroll, bank, Savings Plan, ESOP, trust, stock-purchase, valuation, accounting, tax, and communication records.

XVII. Bottom-Line Control Statement

The fully integrated sequence is:

National PPP / ERISA universe → repaired comparison universe → four-gate reduction → Selway alone → PPP principal of $4,885,300 → near-total payroll coding of $4,885,297 → Second Draw of $2,000,000 → exact 60% threshold of $1,200,000 → 2021 ESOP employer contribution receivable of $1,200,000 → PPP remainder after ESOP of $3,685,300 → 2021 Savings Plan distributions of $3,712,289 → combined ERISA / ESOP vector of $4,912,289 → $26,989 difference from PPP principal → 2022 ESOP receivable clearance → 2022 ESOP purchase of $2,330,000 in Selway common stock → 7,781.75-share movement tie-out → non-eligible PPP payroll-cost classification as shown → primary-document reconciliation demand.

This is the singular integrated memorandum.

Integrated Property, Rent, Minority-Interest, and Control-Side Liquidity Pathway

Current status: the property instruments are locked public-record facts. Ownership percentage,

sale price, property value, rent entitlement, distress, buyout funding source, and any direct PPP/plan/ESOP

connection remain unresolved. The 35% ownership figure and calculator inputs are assumptions, not findings.

A. Locked public-record property structure

- Alameda County recording nos. 2001498182 (December 21, 2001),

20022741238 (May 31, 2002), and 2003255868 (May 1, 2003)

concern 29250 Union City Boulevard and assignments of leases, rents, issues, and profits.

- The 2001 and 2003 instruments expressly connect secured obligations to Selway Machine Tool Co., Inc.

- Official Record no. 2003255868, PDF page 2, Article II §2.01(a), references a February 1, 2003

continuing guaranty securing Selway-related obligations up to $8,000,000 in principal,

plus interest, fees, and other amounts.

B. Why this pathway belongs in the integrated analysis

The property lane is not included because the public record proves that PPP, Savings Plan, or ESOP funds

purchased a property interest. It is included because the documented property/rent relationship and the

unresolved minority-interest transaction create two additional trace endpoints: the source of buyout funds

and the fairness of the price. Those endpoints test whether independently documented liquidity events remained

separate or converged into a control-side acquisition.

| Transaction lane | Documented fact or current input | Unresolved connection |

|---|

| Property / rents |

Recorded instruments tied the Union City property and rents to Selway-related secured obligations. |

Actual ownership, rent rights, enforcement, and whether rent pressure affected a seller’s decision. |

| Minority-interest transaction |

The application treats a minority-interest buyout as a required trace endpoint. |

Sale price, buyer, seller, escrow, wire source, deposit destination, and independent capital source. |

| Savings Plan liquidity |

$3,712,289 in 2021 benefit distributions. |

Recipients, dates, deposits, downstream transfers, and whether any funds reached buyer/property/control accounts. |

| ESOP liquidity |

$1,200,000 receivable no longer outstanding by 2022; $2,330,000 employer-stock purchase. |

Receivable resolution, seller/payee, bank path, and whether stock-sale liquidity reached a buyout or control-side transaction. |

| PPP-enabled corporate liquidity |

$4,885,300 principal and $4,933,228.76 forgiveness. |

Whether eligible payroll independently supported forgiveness and whether PPP relief indirectly freed other funds for a control event. |

C. Benign independent-trails explanation — what must be true

- PPP forgiveness must be independently supported by eligible payroll/payment records.

- Savings Plan distributions must trace to lawful participants/beneficiaries without buyer/property/control-side downstream flow.

- The ESOP stock purchase must identify a lawful seller/payee, adequate consideration, independent valuation, and prudent trustee process.

- Any minority-interest purchase must be funded by independently documented capital or financing unrelated to PPP, plan, or ESOP proceeds.

- The sale price and rent assumptions must be supported by independent appraisal, market data, documented discounts, and uncoerced consent.

D. Facts that activate the integrated control-side theory

- A Savings Plan recipient, ESOP stock seller/payee, related party, buyer, escrow, or property account overlaps.

- The buyer’s funds cannot be traced to independent capital or financing.

- PPP-supported liquidity, plan distributions, the ESOP receivable, or stock-sale proceeds are directly or indirectly used in the acquisition.

- The price lacks independent valuation or reflects rent-pressure distress, suppressed rent, conflicted authority, or an unsupported discount.

- Records are missing, contradictory, altered, backdated, or withheld after the issue became known.

E. Exact records required

| Question | Primary records |

|---|

| Who owned what? | Deeds, title reports, trust/estate records, operating agreements, stock/property ledgers, ownership schedules. |

| What was bought and for how much? | Purchase agreement, amendments, escrow closing statement, settlement sheet, seller statement, tax reporting. |

| Who funded it? | Buyer bank statements, wire confirmations, loan documents, related-party transfers, source-of-funds declaration, escrow ledger. |

| Was price fair? | Independent appraisal, valuation workbook, market-rent comparables, minority/marketability discount analysis, fairness review. |

| Was consent free from pressure? | Lease/rent ledger, rent demands, communications, notices, trustee/fiduciary minutes, seller-side advice and authority records. |

| Did funds converge? | PPP accounts, payroll accounts, Savings Plan trust statements, 1099-Rs, ESOP trust accounts, stock-purchase wires, escrow and recipient accounts. |

Open the assumption-based fair-price/rent calculator ·

Open focused record demands ·

Open evidence intake ·

Back to Executive Decision Brief

Addendum — Worst-Case Legal Exposure Memorandum

Integration with the earlier analytical body

This legal-exposure addendum is conditional and should be read together with the earlier sections that separate locked facts, unresolved questions, and scenario-dependent exposure.

PPP / ERISA / ESOP / Savings Plan / Fiduciary-Duty Exposure Analysis

Subject: Legal exposure if the Selway PPP proceeds or forgiveness support were proven to have been materially misclassified, diverted, double-counted, or substituted through Savings Plan distributions, ESOP receivable treatment, and ESOP stock-purchase mechanics.

Control assumption: This addendum assumes the worst-case factual scenario for analytical purposes only: that the PPP money or PPP-forgiveness support was found not to have been consumed in eligible payroll costs, but instead was materially connected to non-payroll Savings Plan distributions, an ESOP employer-contribution receivable, and/or ESOP stock purchases. The integrated memorandum’s public-record premise is that Selway’s PPP principal was $4,885,300, total forgiveness was $4,933,228.76, public payroll-coded proceeds were $4,885,297, the 2021 ESOP showed a $1,200,000 employer contribution receivable, the 2021 Savings Plan showed $3,712,289 in benefit distributions, and the 2022 ESOP showed a $2,330,000 purchase of 7,781.75 shares of Selway common stock.

I. Executive Exposure Conclusion

If the worst-case concern scenario were proven true, the exposure would not be limited to an accounting error or a Form 5500 classification issue. It would implicate four interconnected federal regimes:

PPP / SBA / Treasury exposure — false borrower certifications, false forgiveness certifications, false payroll-cost classification, failure to satisfy the 60% payroll-cost rule, and improper forgiveness of federal debt.

False Claims Act exposure — civil liability for knowingly obtaining or retaining federal money through false claims, false records, material omissions, or reverse false claims. The False Claims Act imposes treble damages plus civil penalties for knowingly false claims to the United States, and “knowingly” includes actual knowledge, deliberate ignorance, or reckless disregard; no specific intent to defraud is required.

Criminal fraud / false statement exposure — potential exposure under wire fraud, bank fraud, false statements, false claims, false loan-application statements, conspiracy, money laundering, ERISA false-statement statutes, and employee-benefit-plan embezzlement/conversion statutes, depending on proof of intent, routing, representations, bank transmissions, and plan-asset use. Wire fraud and mail fraud tied to a presidentially declared emergency, or affecting a financial institution, can carry up to 30 years’ imprisonment and a $1,000,000 fine; bank fraud carries the same maximum.

ERISA / ESOP / fiduciary-duty exposure — breach of loyalty, breach of prudence, prohibited transactions, party-in-interest transactions, ESOP overpayment or valuation issues, improper use of plan assets, false or incomplete plan records, fiduciary removal, restoration of plan losses, disgorgement of fiduciary profits, civil penalties, and IRS excise taxes. ERISA fiduciaries must act solely in the interest of participants and beneficiaries and for the exclusive purpose of providing benefits and paying reasonable plan expenses.

The central point is this: if the integrated public-record pattern were confirmed by primary records as an actual misuse or false-support pathway, then the matter would become a federal civil-fraud, criminal-fraud, ERISA fiduciary-breach, prohibited-transaction, tax, and corporate-governance exposure event.

II. Worst-Case Fact Pattern Being Tested

The worst-case scenario is not merely that the public records show suspicious convergence. The worst-case scenario is that primary records prove some or all of the following:

- PPP applications or forgiveness applications certified payroll costs that were not actually paid or incurred as eligible payroll costs.

- PPP forgiveness was supported by non-payroll categories while publicly coded as almost entirely payroll.

- Savings Plan benefit distributions were treated, directly or indirectly, as payroll-cost support or as a substitute for payroll.

- The $1,200,000 ESOP employer contribution receivable was counted as a PPP-eligible retirement contribution even though it was not actually paid within the required covered-period/payment framework.

- The $1,200,000 ESOP component was used because it matched exactly 60% of the $2,000,000 Second Draw, thereby satisfying the threshold arithmetically without satisfying the legal category.

- The $2,330,000 ESOP stock purchase was part of the same economic pathway, clearing or transforming the ESOP receivable into employer-stock acquisition rather than eligible payroll support.

- Corporate officers, fiduciaries, trustees, plan administrators, accountants, payroll providers, or lenders knew, ignored, or recklessly disregarded the mismatch between PPP payroll certifications and ERISA/ESOP transaction reality.

- Plan participants, the ESOP, the Savings Plan, the SBA, the lender, or the United States Treasury suffered loss or were deprived of accurate decision-critical information.

If those facts were proven, the exposure would turn on materiality, knowledge, intent, documentation, timing, and role allocation.

III. PPP / SBA / Treasury Exposure

PPP funds were designed to support payroll costs and certain limited nonpayroll costs. Treasury described the program as providing funds to pay payroll costs, including benefits, with additional permitted uses such as mortgage interest, rent, and utilities. SBA Form 3508 remains the central forgiveness form for loans over $150,000, and SBA identifies Form 3508 and its instructions as the forgiveness application and instructions for PPP borrowers.

In the worst-case scenario, the PPP problem would have three layers.

A. False use-of-proceeds / false forgiveness support

If Selway represented that the loan proceeds or forgiveness support were payroll costs, but the supporting economic events were actually Savings Plan distributions, ESOP receivables, or employer-stock purchases, the core exposure would be:

- false payroll-cost classification;

- false retirement-plan contribution classification;

- false documentation of paid or incurred costs;

- false certification of forgiveness eligibility;

- possible ineligibility for full forgiveness;

- possible obligation to repay forgiven amounts;

- possible administrative referral to SBA OIG, DOJ, Treasury, IRS, and DOL EBSA.

The integrated memorandum states that the public PPP record shows $4,885,297 payroll-coded proceeds against $4,885,300 principal, leaving only $3 outside payroll coding. If that near-total payroll coding were proven false or materially unsupported, the exposure would attach to the entire forgiveness architecture.

B. 60% payroll-cost threshold exposure

The Second Draw was $2,000,000, making the 60% threshold $1,200,000. The 2021 ESOP receivable was also $1,200,000. If the ESOP receivable was used to satisfy or help satisfy the 60% payroll-cost rule, the legal issue would be severe because a receivable is not the same thing as a paid or properly incurred eligible payroll cost.

The exposure theory would be:

The borrower reached the forgiveness threshold numerically by using a retirement-plan number that exactly matched the statutory/payroll threshold, while the actual ERISA category was a receivable or employer-stock pathway rather than documented covered-period payroll expenditure.

That would be materially different from a clerical error. It would be a category-substitution theory.

C. Administrative remedies

SBA could seek denial, reversal, repayment, administrative collection, debarment-type consequences, lender-file review, referral to SBA OIG, and referral to DOJ. The PPP itself has ended, but SBA still identifies existing borrowers as potentially eligible for forgiveness and maintains PPP loan-forgiveness resources.

IV. False Claims Act Exposure

The False Claims Act is the primary civil-fraud statute for federal money. It reaches knowingly false claims, false records material to claims, conspiracy, and improper avoidance of repayment obligations. DOJ describes the FCA as imposing treble damages and penalties on those who knowingly and falsely claim money from the United States or knowingly fail to pay money owed to the United States.

A. Potential FCA theories

If the worst-case facts were proven, FCA theories could include:

- False claim for forgiveness — submitting PPP forgiveness applications that falsely represented eligible payroll costs.

- False record or statement — using payroll schedules, retirement-plan support, accounting records, forgiveness worksheets, or lender submissions that were materially false.

- Implied false certification — seeking forgiveness while impliedly certifying compliance with PPP eligibility and payroll-cost rules.

- Reverse false claim — improperly retaining forgiven PPP funds after knowing the forgiveness was unsupported.

- Conspiracy — coordinated action among corporate officers, accountants, plan fiduciaries, trustees, or other actors to obtain or retain federal money.

The FCA’s knowledge standard is critical: it includes actual knowledge, deliberate ignorance, and reckless disregard, and does not require proof of specific intent to defraud. That means a “we did not intend fraud” defense would not end the analysis if the evidence showed reckless disregard of obvious category, timing, or documentation mismatches.

B. Monetary exposure

Using the integrated memo’s figures:

- PPP principal: $4,885,300

- PPP forgiveness: $4,933,228.76

- Combined ERISA / ESOP vector: $4,912,289

If the government treated the full forgiveness amount as improperly obtained, the FCA damages base could be approximately $4.93 million. Treble damages could place the civil damages exposure near $14.8 million, before civil penalties, costs, interest, settlement multipliers, or collateral administrative consequences. The FCA statute also provides civil penalties per false claim or false record, adjusted for inflation.

A more limited theory could use a smaller damages base, such as the unsupported Second Draw portion, the $1.2 million ESOP component, or the delta between actual eligible payroll and forgiven amount. But the worst-case exposure is full-forgiveness disgorgement plus trebling.

C. Individual and entity exposure

The corporate entity would be exposed as the borrower. Individuals could be exposed if they caused, approved, certified, prepared, transmitted, or knowingly participated in the false claim. Accountants, consultants, payroll providers, trustees, or plan administrators are not automatically liable merely because they touched records, but they can become exposed if evidence shows knowing participation, reckless disregard, or false-record causation.

V. Federal Criminal Exposure — PPP Fraud, False Statements, and Financial Institution Fraud

The criminal exposure depends on proof beyond a reasonable doubt and proof of intent or knowledge under the specific statute. But if the worst-case scenario were proven, the following criminal statutes would be in play.

A. Wire fraud — 18 U.S.C. § 1343

PPP applications, forgiveness applications, lender communications, ACH transfers, electronic submissions, payroll records, and plan records typically involve interstate wires. Wire fraud can apply where a scheme to defraud used interstate electronic communications. Where the violation relates to a benefit connected to a presidentially declared emergency, or affects a financial institution, the statute provides up to 30 years’ imprisonment and a $1,000,000 fine.

Worst-case theory:

Electronic PPP submissions and forgiveness documentation were used to obtain or retain federal funds through materially false payroll-cost and retirement-plan representations.

B. Bank fraud — 18 U.S.C. § 1344

PPP loans were processed through lenders. If false information was used to influence or defraud a participating financial institution, bank fraud exposure could arise. Bank fraud carries up to 30 years’ imprisonment and a $1,000,000 fine.

Worst-case theory:

The lender was induced to approve, process, or forgive PPP obligations based on false payroll, retirement contribution, or use-of-proceeds representations.

C. False statements to federal agencies — 18 U.S.C. § 1001

If a borrower or responsible person knowingly and willfully made materially false statements in a matter within federal jurisdiction, § 1001 could apply. The statute generally provides up to 5 years’ imprisonment.

Worst-case theory:

SBA-facing certifications, forgiveness representations, or supporting documents falsely stated that funds were used for eligible payroll costs.

D. False loan statements — 18 U.S.C. § 1014

Section 1014 reaches knowingly false statements or willful overvaluations made for the purpose of influencing specified lending institutions and federal credit-related actors.

Worst-case theory:

Loan or forgiveness submissions falsely represented payroll costs, headcount, compensation, retirement-plan costs, or covered-period support to influence PPP lending or forgiveness action.

E. False claims — 18 U.S.C. § 287

A criminal false-claims theory could apply if a claim against the United States was knowingly false, fictitious, or fraudulent. Section 287 provides up to 5 years’ imprisonment.

Worst-case theory:

The forgiveness request was a knowingly false claim against the United States because it sought cancellation of debt based on ineligible or falsely characterized costs.

F. Mail fraud — 18 U.S.C. § 1341

If mailed documents were used in the scheme, mail fraud may apply. Like wire fraud, mail fraud tied to emergency-benefit funds or affecting a financial institution can carry up to 30 years’ imprisonment and a $1,000,000 fine.

G. Conspiracy — 18 U.S.C. § 371 or § 1349

If multiple actors agreed to defraud the United States or commit fraud offenses, conspiracy exposure could arise. Section 1349 provides that attempts and conspiracies to commit offenses under the federal fraud chapter carry the same penalties as the underlying offense.

H. Money laundering — 18 U.S.C. § 1956

If proceeds of unlawful activity were moved through accounts or transactions to conceal source, ownership, control, or nature, money-laundering exposure could arise. Section 1956 can carry up to 20 years’ imprisonment and fines of up to $500,000 or twice the value of the property involved, depending on the subsection.

Worst-case theory:

PPP proceeds or fraud proceeds were moved through payroll, plan, ESOP, receivable, stock-purchase, or related-party channels to disguise non-payroll use.

This theory would require more than mere spending. It would require evidence of concealment, specified unlawful activity proceeds, or prohibited transactional intent.

VI. ERISA Fiduciary-Duty Exposure

The ERISA exposure is distinct from PPP exposure. PPP asks whether federal loan proceeds and forgiveness were supported by eligible costs. ERISA asks whether plan fiduciaries acted solely in participants’ interests, prudently, loyally, and without prohibited conflicts.

ERISA fiduciaries must discharge duties solely in the interest of participants and beneficiaries, for the exclusive purpose of providing benefits and defraying reasonable plan expenses. Fiduciaries must also act prudently, and prudence focuses on the decision-making process and documentation of that process.

A. Breach of loyalty

If ESOP or Savings Plan transactions were structured to solve the company’s PPP-forgiveness problem, rather than to benefit plan participants, that would strike at ERISA’s duty of loyalty.

Worst-case loyalty breach:

Plan mechanics were used for corporate financing, PPP forgiveness optics, shareholder liquidity, or insider benefit, rather than for the exclusive benefit of plan participants.

B. Breach of prudence

If fiduciaries accepted, approved, or failed to investigate a $1.2 million receivable, a $2.33 million employer-stock purchase, or related valuation assumptions without independent review, adequate documentation, or conflict controls, prudence exposure would arise. DOL has specifically emphasized that ESOP trustees must ensure an ESOP pays no more than fair market value for employer stock and has pursued cases alleging inadequate due diligence and overpayment in ESOP stock transactions.

C. Prohibited transactions

ERISA prohibits fiduciaries from causing plans to engage in certain transactions with parties in interest, including sales or exchanges of property, lending or extensions of credit, transfers or use of plan assets for the benefit of a party in interest, and certain acquisitions of employer securities.

Worst-case prohibited-transaction theories:

- ESOP purchase of employer stock from a party in interest at more than adequate consideration.

- Extension of credit or receivable treatment between the plan and employer.

- Use of plan assets to benefit the employer, selling shareholders, fiduciaries, or related parties.

- Plan transaction used to satisfy corporate PPP or liquidity needs.

- Savings Plan distributions coordinated to create non-plan corporate benefit.

ERISA does contain exemptions, including exemptions related to qualifying employer securities and certain ESOP transactions, but exemption status would depend on strict compliance with statutory conditions, adequate consideration, fiduciary process, valuation, and absence of disqualifying conflict. DOL and Treasury coordination is built into ERISA’s exemption framework.

D. Fiduciary personal liability

If fiduciary breach is proven, ERISA makes fiduciaries personally liable to restore plan losses, return fiduciary profits made through use of plan assets, and face equitable or remedial relief, including removal.

This is a major individual-exposure point. The plan sponsor may be exposed, but fiduciaries themselves may also face personal liability.

E. ERISA civil penalties

ERISA civil enforcement can include DOL actions, participant/beneficiary actions, fiduciary actions, equitable relief, and penalties. For certain fiduciary breaches or knowing participation in breaches, the Secretary of Labor must assess a civil penalty equal to 20% of the applicable recovery amount, subject to statutory waiver or reduction conditions.

For prohibited transactions by parties in interest, ERISA also permits civil penalties up to 5% of the amount involved for each year or part of a year during which the transaction continues, and up to 100% of the amount involved if not corrected after notice.

VII. ESOP-Specific Exposure

The ESOP stock-purchase pathway is especially sensitive because ESOPs are permitted to hold employer securities, but the fiduciary and valuation standards are strict.

A. Adequate consideration / valuation exposure

If the ESOP paid $2,330,000 for Selway common stock, the central ESOP question becomes whether the ESOP paid no more than fair market value, whether the valuation was independent and reliable, whether the trustee prudently investigated the valuation, and whether any seller, officer, trustee, or fiduciary conflict affected the transaction.

Worst-case ESOP stock exposure:

- The ESOP overpaid for employer stock.

- The valuation was inflated to accommodate corporate finance or shareholder liquidity.

- The trustee failed to conduct adequate due diligence.

- The ESOP transaction was linked to clearing the $1.2 million receivable rather than independent plan benefit.

- The transaction benefited selling shareholders, the company, or insiders more than participants.

DOL’s ESOP enforcement position has repeatedly focused on whether ESOP trustees approved transactions without required due diligence and caused ESOPs to overpay for employer stock.

B. Receivable as credit / contribution issue

The 2021 ESOP receivable presents a separate problem. If the receivable was booked as a contribution but not paid, and then later cleared through a stock-purchase pathway, the issues become:

- Was the receivable legally enforceable?

- Was it timely paid?

- Was it offset, netted, forgiven, converted, or satisfied through another transaction?

- Did the ESOP receive cash, property, stock, or merely accounting treatment?

- Was the receivable used as PPP forgiveness support?

- Did the receivable benefit participants or the employer?

- Was it properly disclosed on Form 5500 and plan financials?

If the receivable was used to support PPP forgiveness while remaining unpaid at year-end, the same fact could have consequences in both systems: PPP false-support exposure and ERISA fiduciary/prohibited-transaction exposure.

VIII. Savings Plan Exposure

The Savings Plan lane involves the $3,712,289 benefit distribution. The integrated memo emphasizes that this amount was a plan outflow to participants or beneficiaries, not an employer contribution.

A. Distribution legitimacy

If the distributions were ordinary participant distributions, properly authorized, paid to participants, reported on Forms 1099-R, and unrelated to PPP support, the Savings Plan lane may be benign.

But under the worst-case assumption, exposure arises if:

- distributions were accelerated, induced, coordinated, or structured for non-participant corporate purposes;

- distributions were used to create a misleading payroll-cost proxy;

- distributions were incorrectly represented to SBA or lenders as borrower-paid payroll or retirement contribution costs;

- distribution records were incomplete, false, backdated, or misleading;

- participants were pressured or disadvantaged;

- plan assets were used for employer or insider benefit.

B. Criminal plan-asset exposure

If any plan assets were unlawfully converted, abstracted, or used for someone else’s benefit, 18 U.S.C. § 664 becomes relevant. That statute applies to anyone who embezzles, steals, or unlawfully and willfully converts money, funds, securities, credits, property, or other assets of an employee benefit plan, and provides up to 5 years’ imprisonment.

This would require proof of plan-asset misuse. The mere fact of a large distribution is not enough. But if distributions were false, coerced, routed, or diverted, the exposure becomes criminal.

IX. ERISA False Statements and Plan-Record Exposure

If plan records, Form 5500 filings, certifications, audit records, trustee records, or plan-administrator records were false or concealed material facts, 18 U.S.C. § 1027 becomes relevant. That statute covers false statements or concealment of facts in documents required by ERISA to be published, kept as plan records, or certified to a plan administrator, and provides up to 5 years’ imprisonment.

Worst-case theories:

- Form 5500 filings mischaracterized receivables, contributions, distributions, or party-in-interest transactions.

- ESOP records concealed the real purpose or funding source of the stock purchase.

- Savings Plan records concealed distribution routing or participant impact.

- Plan records were made incomplete so that the PPP/ERISA reconciliation could not be verified.

- Amendments or later filings attempted to obscure the original transaction sequence.

DOL EBSA states that it conducts investigations of criminal violations involving employee benefit plans, including embezzlement, kickbacks, and false statements under Title 18, with prosecutions handled by U.S. Attorneys’ offices.

X. IRS / Tax Exposure

The tax layer would depend on deductions, timing, contribution treatment, payroll tax reporting, plan qualification, and treatment of ESOP/Savings Plan transactions.

A. Improper deductions

If a company deducted retirement contributions that were not actually paid, were improperly accrued, were not ordinary and necessary business expenses, or were connected to nonqualified/prohibited transactions, IRS exposure could arise. Section 162 generally allows deductions for ordinary and necessary business expenses paid or incurred in carrying on a trade or business, but the facts would determine whether the claimed expense was valid.

B. Prohibited-transaction excise taxes

For prohibited transactions, IRS rules impose excise taxes on disqualified persons. IRS states that a disqualified person must pay an initial tax of 15% of the amount involved for each year or part of a year in the taxable period, and if the transaction is not corrected, an additional tax of 100% of the amount involved can apply.

Applied to the worst-case numbers:

- If the amount involved were $1,200,000, the initial 15% excise tax would be $180,000 per applicable year or part-year, with possible 100% additional tax of $1,200,000 if uncorrected.

- If the amount involved were $2,330,000, the initial 15% excise tax would be $349,500 per applicable year or part-year, with possible 100% additional tax of $2,330,000 if uncorrected.

- If multiple transactions were involved, the exposure could stack.

C. False tax return / false document exposure

If tax returns, deductions, contribution schedules, Forms 1099-R, corporate returns, plan filings, or related books were willfully false, criminal tax statutes could become relevant. Section 7206 provides felony exposure for fraud and false statements, with fines up to $100,000 for individuals, $500,000 for corporations, imprisonment up to 3 years, or both, plus costs of prosecution.

XI. Corporate Entity Exposure

For the corporate entity, the worst-case exposure includes:

- repayment of PPP forgiveness;

- False Claims Act treble damages;

- civil penalties per false claim or false record;

- SBA administrative collection;

- interest and costs;

- possible suspension, debarment, or loss of government-contracting eligibility;

- criminal fines;

- restitution;

- forfeiture exposure if criminal proceeds are traced;

- lender claims;

- indemnification disputes;

- D&O insurance disputes;

- audit restatements;

- tax adjustments;

- ERISA co-fiduciary or knowing-participation exposure if the company acted in a fiduciary or party-in-interest capacity;

- reputational and transactional impairment.

The corporate entity’s largest civil exposure would likely be FCA-based: approximately treble the improperly forgiven amount, plus penalties, interest, and costs. If the damages base is the full $4,933,228.76 forgiveness amount, the treble-damages figure is approximately $14,799,686.28, before penalties and ancillary exposure.

XII. Individual Exposure

Individual exposure depends on role, knowledge, signature authority, fiduciary status, and participation.

A. Corporate officers and signatories

Officers who signed PPP applications, forgiveness applications, payroll certifications, accounting records, or lender submissions could face:

- FCA liability if they caused false claims;

- criminal false-statement exposure;

- wire fraud or bank fraud exposure;

- conspiracy exposure;

- tax false-statement exposure;

- corporate indemnification disputes;

- D&O coverage disputes;

- potential personal restitution.

B. Plan fiduciaries

Savings Plan or ESOP fiduciaries could face:

- personal liability to restore plan losses;

- disgorgement of profits;

- removal as fiduciaries;

- DOL penalties;

- prohibited-transaction penalties;

- IRS excise taxes if they are disqualified persons participating in prohibited transactions;

- criminal exposure if plan assets were knowingly converted or plan records falsified.

ERISA fiduciary personal liability is direct: a breaching fiduciary is personally liable to make good plan losses and restore profits made through use of plan assets.

C. ESOP trustee

The ESOP trustee’s exposure would be especially acute if the stock purchase was overvalued, conflicted, inadequately investigated, or linked to corporate PPP needs. DOL’s ESOP enforcement focus on trustee due diligence and fair-market-value protection makes the trustee’s process, independence, valuation review, and conflict controls central.

D. Accountants, advisors, payroll providers, plan administrators

Advisors are exposed if they knowingly prepared, certified, transmitted, or caused false records. They are less exposed if they acted on incomplete information without knowledge or reckless disregard. The key issue is whether they were neutral recordkeepers or knowing participants.

XIII. Lender Exposure

The lender’s exposure depends on whether it acted in good faith, followed SBA rules, or knowingly ignored red flags. If the lender merely processed borrower-submitted information in accordance with PPP procedures, lender exposure may be limited. But if lender personnel knew the payroll support was false, ignored obvious contradictions, or helped structure the false support, exposure could include FCA causation, bank-record issues, SBA guaranty issues, and regulatory scrutiny.

The lender review file is therefore central. It would show what was submitted, what was questioned, what was accepted, and whether the mismatch between payroll coding and ERISA/ESOP categories was visible.

XIV. Obstruction, Concealment, and Spoliation Exposure

If, after the fact, records were altered, withheld, deleted, backdated, or misleadingly amended, exposure could expand beyond the original PPP/ERISA issues.

Relevant evidence would include:

- original PPP applications;

- original forgiveness submissions;

- lender questions and borrower responses;

- payroll registers;

- bank statements;

- accounting journal entries;

- ESOP receivable schedules;

- stock-purchase agreements;

- valuation reports;

- board minutes;

- trustee approvals;

- Form 5500 original and amended filings;